The Printing Industry Takes First Steps Toward Recovery

Key printing industry business indicators are showing improvement, according to a recent NAPCO Research/PRINTING United Alliance survey. Improvement is over the deepest days of the COVID-19 crisis, and activity is still far below what is normal for this time of the year. But movement off bottom is the first step toward recovery. From early May through early June, our industry took that step.

The survey is part of our COVID-19 Print Business Indicators Research program. The program investigates the economic effects of the pandemic on the printing industry, how printers are responding, and how they can create a path forward. More than 450 companies, including commercial printers, graphic and sign producers, apparel decorators, functional printers, and package printers/converters, participated.

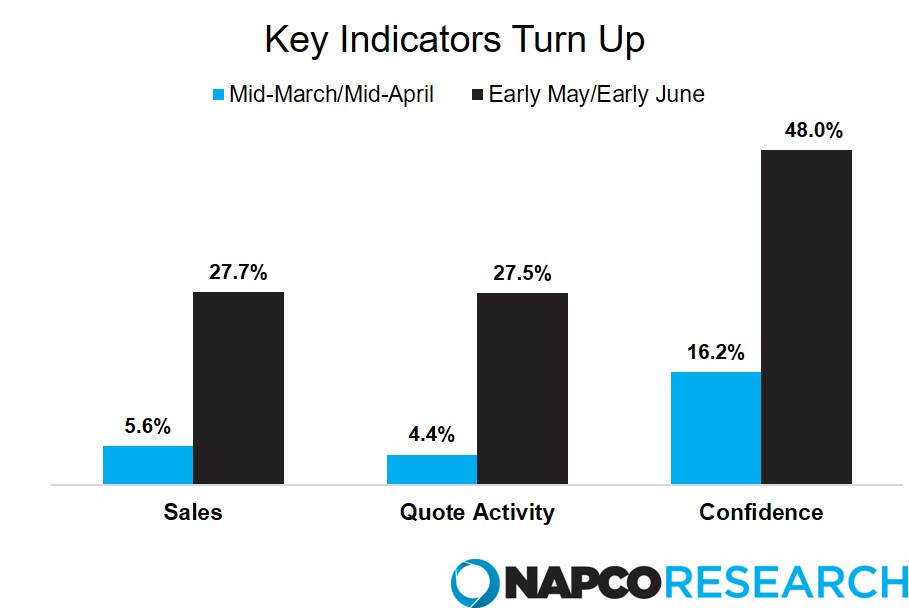

Among all companies surveyed, sales fell 30.2%, on average, from early May through early June, increasing for 17.8% and decreasing for 73.1%. But two months earlier, sales fell an average of 53.7%, increasing for 4.3% and decreasing for 89.5%. As the chart below shows, sales are trending higher for 27.7%, up from 5.6%, quote activity is trending higher for 27.5%, up from 4.4%, and 48% expect business to improve during the month ahead, triple early spring’s 16.2%.

Q. Percent of participants in the NAPCO Research/PRINTING United Alliance COVID-19 Print Business Indicators Survey reporting sales are trending up, quote activity is trending up, and expecting business to improve during the month ahead n=449. Click to enlarge.

Many we surveyed question whether the uptick is sustainable. An apparel decorator “expects the trend to continue upwards,” but adds, “It is very difficult to assess given so many outside variables and uncertainty. Also, we believe the trend up will be painfully slow and possibly take 18 months.”

A commercial printer reports, “Our sales started dropping on March 13. We hit bottom on April 9. We bounced along the bottom until May 11, when order writing came off the bottom at an increasing rate. It’s impossible to declare a long-term trend from this small data set.”

Companies in every printing segment studied commented on how customers are reopening but “taking a wait-and-see attitude” and on how cloudy the outlook really is: “With talk of a second wave in the fall, and also with PPP and EIDL funds running out before then, I would say we're more hopeful than confident.”

So, what is ahead? Expect the economy to give our industry a boost — but not until 2021. Unprecedented monetary and fiscal stimulus is in place, with more coming. There is also pent-up demand for everything we haven’t been able to do in months. But because this recession is rooted in biology, not economics, the ultimate cure will be biological, i.e., effective, widespread testing and a vaccine. Neither is likely until next year. In the meantime, social distancing, restrictions on business operations, and other realities of the pandemic will continue to encumber the economy.

Also expect the recovery to leave many printing companies behind. Our recoveries used to be inclusive; survive the contraction and ride the expansion up. Now they are increasingly exclusive, limited to companies best prepared for an environment defined by the following:

- Expanding opportunity but shrinking margin for error. Opportunity to get involved in clients’ work earlier, stay involved longer, and satisfy a broader range of their communication needs will continue to grow. But so will competition, as print providers migrate into adjacent product categories. Please click the link to view our Convergence in the Print Industry report.

- Abrupt, disruptive change. The fourth Great Economic Revolution, driven by artificial intelligence, robotics, the Internet of things, rich data, and 3D printing, is redefining our technology, clients, competition, critical skills, labor force, value proposition, and everything else that matters.

- Pressure to do more and faster. It’s not just getting faster at printing work. Clients want more services, from database management to multimedia communications programs. That creates more process steps and room for error. Print providers that take action to automate workflow, reduce bottlenecks, minimize steps and touches, eliminate processes that no longer add value, and better manage inventory management will be in the best position to weather turbulent business conditions that lie ahead.

For the recovery ahead, add one more factor: increased macroeconomic volatility. The Federal Reserve and Washington will eventually have to unwind the stimulus they’ve created. It will be a historic experiment on quantities beyond anything they’ve ever had to manage. How much of a drawdown will be just enough? No one knows. And that will create volatility.

Who participates fully in the recovery will not be a matter of company size or of offering a particular set of technologies, products, and services. And business fundamentals such as cash management, workforce development, and customer service will not be enough. They are the prerequisites required just to get in the door. Rather, sustained success will require:

- Gathering and analyzing market intelligence. A graphic and sign producer we surveyed credits early identification of the need for PPE and COVID-19 messaging as “key for us.” His sales were up 15% from early May through early June and 5% from mid-March through mid-April. During the same periods, sales were down an average of 17.3% and 52.3%, respectively, for all graphic and sign producers surveyed.

- Acting on the intelligence. Cultivating the agility to move quickly on opportunities and threats identified. A number of participants in our research have moved aggressively into essential industries, home education, home entertainment, etc.

- Execution. Even the best market intelligence and strategic plans aren’t effective if we don’t execute them.

- Opportunity evaluation. Spotting a real opportunity requires considering your company’s specific circumstances, resources, and capabilities to offer it. Understanding what you are getting into makes an immense difference between diversifying and diversifying profitably.

- Rethinking print’s role in communication. Successful providers look beyond how print is manufactured to how print powers communication. Thinking, in particular, about communication that is personalized, integrated with other media, and interactive with mobile devices.

COVID-19 Print Business Indicators Research will continue to provide timely, accurate analysis of the printing industry’s progression through an unprecedented crisis and its aftermath. Access updates at the PRINTING United Alliance and NAPCO Media websites. Please share your thoughts on the reports with our research team at research@napco.com. We’d be delighted to hear from you.

![]()

Analyst Insights features research and analyst insights from the NAPCO and PRINTING United Alliance research teams. Market research is valuable for making strategic business decisions, solving challenges, and pursuing opportunities, and the NAPCO Media research teams survey, analyze, and monitor critical trends related to marketing, printing, packaging, nonprofit organizations, promotional products, and retailing. To learn more about how the team can leverage its research and industry subject matter experts to support your organization’s needs, contact research@napco.com.

- Categories:

- Business Management - Industry Trends

Andrew D. Paparozzi joined PRINTING United Alliance as Chief Economist in 2018. He analyzes and reports on economic, technological, social and demographic trends that will define the printing industry’s future. His most important responsibility, however, is being an observer of the industry by listening to the issues and concerns of company owners, executives and managers. Previously, he worked 31 years at the National Association for Printing Leadership. He has also taught mathematics, statistics and economics at various colleges. Andrew holds a Bachelor’s degree in economics from Boston College and a Master’s degree in economics — with concentrations in econometrics and public finance — from Columbia University.