PRINTING United Alliance Releases State of the Industry Update for Q1 2023

The following article was originally published by Printing Impressions. To read more of their content, subscribe to their newsletter, Today on PIWorld.

The slowdown has started. Fewer participants in PRINTING United Alliance State of the Industry (SOI) research report sales are growing, more report pre-tax profitability is declining, and nearly three-quarters report credit conditions are tightening or that they expect them to later this year.

Even if the slowdown doesn’t degenerate into a full-fledged recession, it will be significant, rewarding the prepared and punishing the unprepared.

The 231 participants in our current survey include commercial printers, graphic and sign producers, apparel decorators, package printers, and functional printers. Annual sales range from less than $500,000 to more than $300 million. Seventy-two percent have diversified beyond their primary printing business.

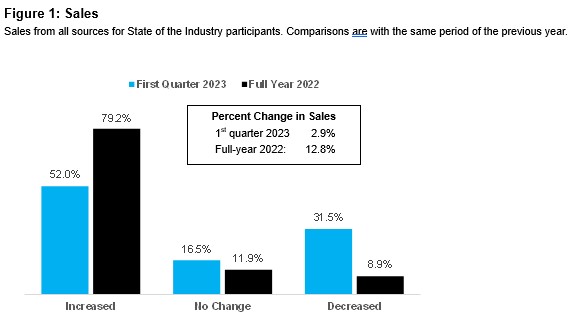

Among all companies surveyed, sales growth slowed to 2.9% during the first quarter of 2023 from 12.8% during full-year 2022. Sales increased for 52.0% and decreased for 31.5%. Last year sales increased for 79.2% and decreased for 8.9%. (See Figure 1.)

Click to enlarge.

Moderating cost inflation explains some of the difference. So far this year operating cost inflation is averaging 6.4% for SOI participants, down from 11.1% last year. Greater supply chain stability is the primary reason for the moderation: Heading into the first half of 2022, 92.3% were very concerned about material shortages and 85.6% were very concerned about rising substrate costs. Heading into the second half of 2023, those numbers are 15.6% and 28.4%, respectively.

But if less cost pass-through were the only difference, real (inflation-adjusted) sales, which measure production by stripping price increases out of dollar sales, would still be growing. They aren’t: Real sales declined 2.0% during the first quarter of 2023 for SOI participants, with reports of decline exceeding reports of increase 51.9% to 39.9%.

Where real sales go, margins soon follow: Companies reporting an increase in margins have fallen to 41.0% of our sample so far this year from 51.4% last year, while companies reporting a decrease have risen to 37.2% from 25.0%.

How our research panel responded to questions about credit conditions, pricing, and overall business conditions is also telling. As Figure 2 shows:

- 5% report credit conditions are tightening (40.8%) or that they expect them to later this year (32.7%).

- 2% report resistance to price increases is growing (48.7%) or that they expect it to later this year (30.5%).

- 3% are already seeing signs of economic slowdown/recession (57.8%) or expect to later this year (31.5%).

Click to enlarge.

Simply put, things are starting to buckle under the weight of the Federal Reserve’s aggressively contractionary monetary policy. The price of credit has risen so rapidly that even the resilient American economy is having trouble adjusting. And because changes in interest rates can take nine months or longer to work through the economy, we are just beginning to see the full effects of the campaign of increases launched in March 2022 – i.e., even if the Fed were to stop raising interest rates, powerful contractionary forces are already in place that will continue to weigh on the economy, and so our industry.

The good news is every economic slowdown/recession creates opportunity. Some markets hold up well and market share and talent become available as the unprepared retreat into survival mode or fail.

Complete results of our survey will be published in the State of the Industry Update, First Quarter 2023, scheduled for June. They include actions such as stepping up risk management and calculating customer health scores that help capture the opportunities slowdowns/recession create; lessons learned from the disruption of the last two years – every market disruption is an opportunity to learn, improve, and be better prepared for the next one – the end markets SOI participants expect to be strongest this year, and sales per employee: What’s typical and what’s exceptional?

PRINTING United Alliance members can download all reports in the State of the Industry Series and nonmembers can download executive summaries at printing.org/library/business-excellence/economics-forecasting/industry-reports. The State of the Industry Series is sponsored by Canon U.S.A., Inc.

Andrew D. Paparozzi joined PRINTING United Alliance as Chief Economist in 2018. He analyzes and reports on economic, technological, social and demographic trends that will define the printing industry’s future. His most important responsibility, however, is being an observer of the industry by listening to the issues and concerns of company owners, executives and managers. Previously, he worked 31 years at the National Association for Printing Leadership. He has also taught mathematics, statistics and economics at various colleges. Andrew holds a Bachelor’s degree in economics from Boston College and a Master’s degree in economics — with concentrations in econometrics and public finance — from Columbia University.