Preview: packagePRINTING Study Reveals How Converters View Printing Technology

The package printing industry has always been one that has relied on innovation and cutting edge equipment to create the most eye-catching products. But in recent years, the advancements in printing technology have been major industry disruptors as printers and converters now have a swath of options at their fingertips to create packaging that would not have been feasible in the past.

With so much new technology being offered to printers, we sought to gain an understanding of the technology they have recently invested in, their near-future investment plans, and the drivers behind these decisions. Throughout May and June, packagePRINTING surveyed its audience of printers and converters across all packaging segments to learn about their recent purchases and future buying intentions.

Digital and Conventional In Tandem

Ever since the emergence of digital printing in the packaging industry, there has been significant debate over whether digital will serve as a replacement for conventional printing technologies such as flexography and offset. However, as printing press suppliers and package printers have come to realize, both technologies have their distinct strengths and are best used in a complementary fashion. The results of this survey support this concept.

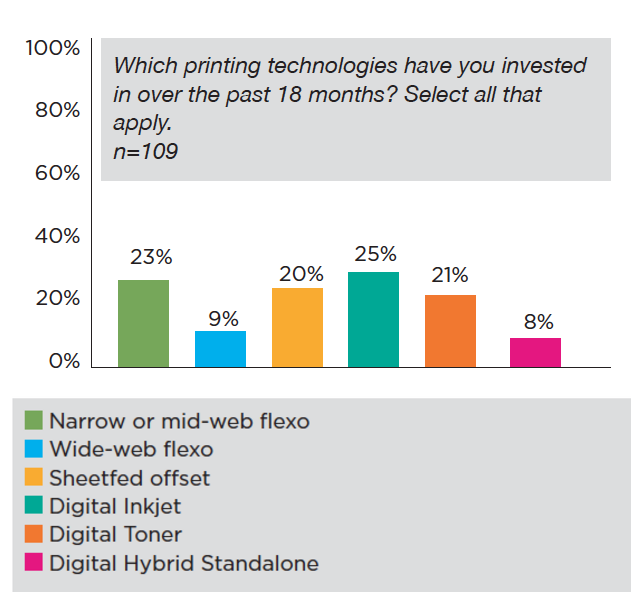

Click to Enlarge.

Prior to asking respondents what printing technology they plan on investing in, we sought to gain an understanding of the printing equipment they have invested in over the past 18 months. The results indicated that investment in digital and conventional printing has been nearly identical in recent years, as 55% of respondents stated they have invested in digital solutions and 53% have invested in conventional printing.

The enthusiasm surrounding digital was in line with our expectations, given that it is a newer technology, with many package printers still in the adoption phase. This is especially true for folding carton, flexible packaging and corrugated printers, where digital printing is still in its early stages as compared to the label segment.

However, what was particularly interesting was the high level of recent investment in conventional printing — especially narrow-web flexography (23%) and sheetfed offset (20%). Flexo and offset are the predominant printing technologies in the label and folding carton segments respectively, and it can be safely assumed that the package printers in these segments have existing presses that they have relied on to be the workhorses of their businesses. However, what these recent investment statistics indicate, is that package printers are seeking out the technological advancements in conventional technology, such as faster speeds, rapid changeovers, increased automation and stronger color control.

While package printers’ recent investments demonstrated a need for both digital and conventional technologies, their future investment plans also support the concept of these being complementary technologies. Half of the respondents said they are likely to invest in digital printing in the next 18 months (25% said they are very likely and 25% said they are somewhat likely), and more than one-third of respondents indicated they were likely to invest in conventional technology (12% very likely, 22% somewhat likely.)

Though there is clearly more enthusiasm for digital printing investment in the near future, the 34% of respondents exploring a conventional investment is significant, and indicates that the need for conventional printing’s strengths is still prevalent, even as digital printing continues its rise in popularity among package printers and their customers.

Investment in Operational Improvement

In an industry where there is constant pressure on package printers to innovate and advance their product line from both a structural and graphical perspective, there is just as much pressure to operate efficiently and help brands get their products to market as quickly as possible. While the latest digital and conventional printing press models have allowed printers and converters to produce exceptionally creative packaging, the results of this survey indicate that for the most part, technological investments are primarily being made with operational efficiency in mind.

This was an interesting trend to see, particularly regarding digital printing investment. Digital printing’s ability to produce variable, customized and personalized output has been well-publicized, as it allows brands to present their products and connect with consumers in ways that were not feasible with conventional printing. And while 69% of respondents indicated this was a key driver of their digital printing investment, it was not No. 1, as 85% of respondents stated that digital printing’s short-run printing capabilities was a key investment driver.

“Being a narrow web house, we find more and more short run work coming in our door,” stated one respondent. “Digital may be a solution to speeding up the short run process if we can make it profitable.”

Meanwhile, the top driver of conventional printing equipment investment is the need for additional capacity, with 59% of respondents selecting this as a top investment driver. This indicates that while the rapid rise of short run work is certainly a major issue for package printers to contend with, the production-length long runs that have been a mainstay of the industry for decades are not going away. And as packaging demand continues to rise, conventional solutions will remain the top choice to produce these runs.

For complete results and analysis from this survey, check out the full report, coming soon.

Cory Francer is an Analyst with NAPCO Research, where he leads the team’s coverage of the dynamic and growing packaging market. Cory also is the former editor-in-chief of Packaging Impressions and is still an active contributor to its print magazines, blogs, and events. With a decade of experience as a professional journalist and editor, Cory brings an eye for storytelling to his packaging research, providing compelling insight into the industry's most pressing business issues. He is an active participant in many of the industry's associations and has played an essential role in the development of the annual Digital Packaging Summit. Cory can be reached at cfrancer@napco.com